Cash flow gaps can quietly slow down even the fastest-growing businesses. That’s where accounts receivable financing comes in—it helps you access cash tied up in unpaid invoices without waiting 30, 60, or even 90 days.

If your revenue looks strong but your bank balance tells a different story, this guide will help you understand how to bridge that gap.

Table of Contents

What Is Accounts Receivable Financing?

Accounts receivable financing is a way for businesses to convert their unpaid invoices into immediate working capital. Instead of waiting for customers to pay, you get most of the invoice value upfront from a financing provider.

Once your customer pays the invoice, the remaining amount is released to you—minus a small fee.

How Does It Work?

Step-by-Step Breakdown

- You issue invoices to your customers

- A financing provider advances a percentage (usually 70–90%)

- Customers pay the invoice as usual

- You receive the remaining balance after fees

It’s simple, fast, and doesn’t require giving up equity.

Why Businesses Use Accounts Receivable Financing

1. Improve Cash Flow Instantly

Instead of waiting weeks or months, you get access to funds within days.

2. Support Business Growth

You can reinvest the cash into inventory, hiring, or expansion opportunities.

3. Avoid Traditional Debt

Unlike loans, this financing is backed by your receivables—not your balance sheet.

4. Handle Seasonal Fluctuations

Perfect for businesses with uneven revenue cycles or long payment terms.

Accounts Receivable Financing vs Factoring

These terms are often used interchangeably, but there’s a difference.

Accounts Receivable Financing

- You retain control of customer relationships

- Customers pay you directly

Invoice Factoring

- The factoring company collects payments

- Customers know you’re using a third party

Choosing between the two depends on how much control you want to maintain.

When Should You Consider It?

Accounts receivable financing works best if:

- You have reliable customers but slow payment cycles

- Your business is growing faster than your cash flow

- You want to avoid taking loans or diluting equity

If late payments are holding you back, this can be a practical solution—not just a temporary fix.

Common Challenges to Watch Out For

1. Cost of Financing

Fees can add up if not managed properly

2. Customer Credit Risk

Your eligibility depends on your customers’ ability to pay

3. Operational Complexity

Manual tracking of invoices can create confusion

This is where having the right systems in place becomes critical.

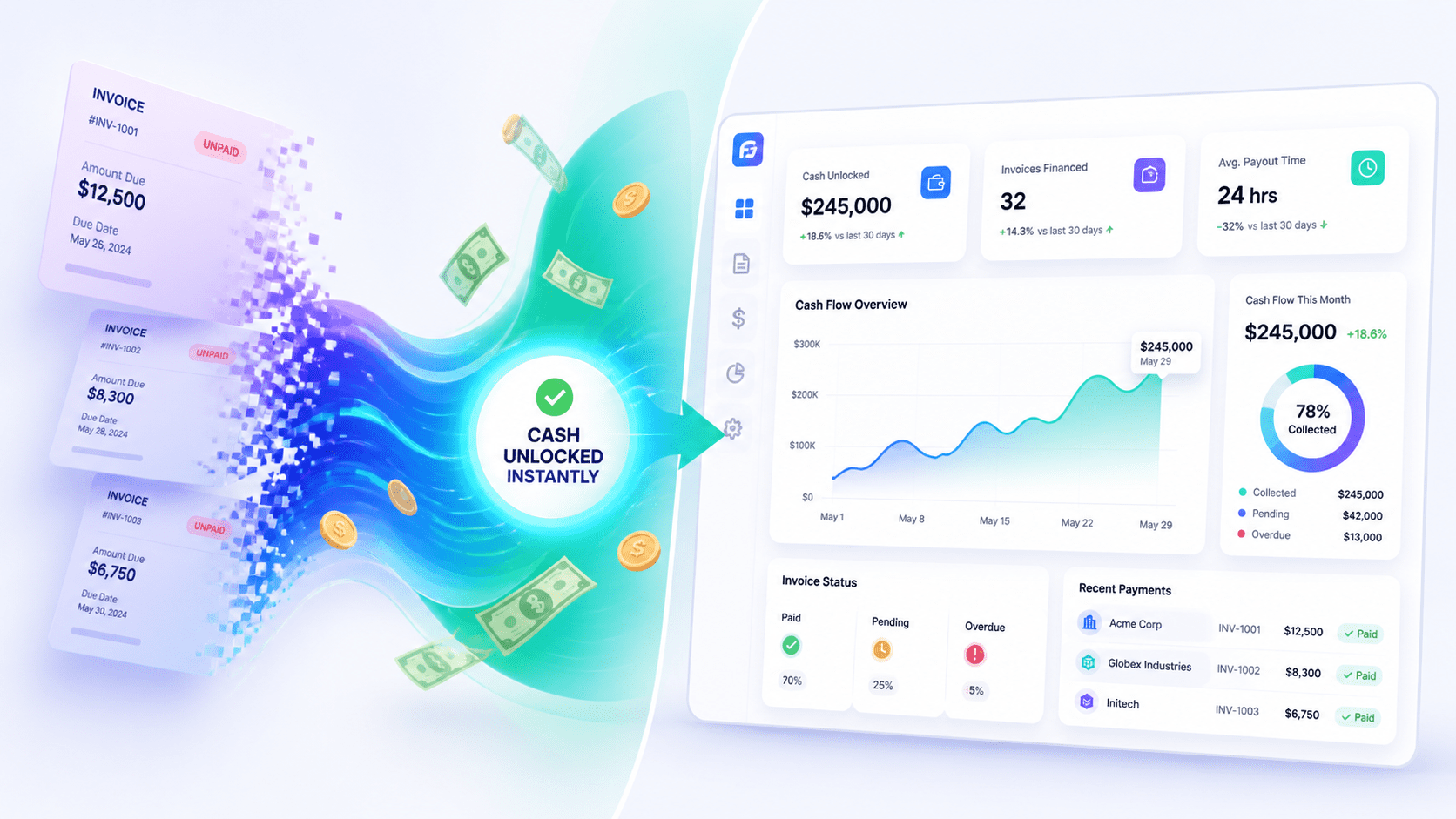

How Technology Makes It Easier?

A vibrant visual illustration of a finance team seamlessly managing invoices on a clean dashboard highlights the shift from manual tracking to automation.

Modern accounts receivable platforms help you:

- Track invoices in real time

- Match payments automatically

- Reduce errors in reconciliation

- Gain full visibility into cash flow

Instead of reacting to cash flow issues, you stay ahead of them.

Is Accounts Receivable Financing Right for You?

It’s not just about accessing funds—it’s about control.

If your business is profitable but constantly short on working capital, accounts receivable financing can give you the flexibility to operate with confidence.

The key is to combine financing with better receivables management so you’re not just solving today’s problem—but preventing tomorrow’s.

About FinFloh

FinFloh is an AI-powered Accounts Receivable platform that helps businesses take control of their cash flow. From automated collections to real-time reconciliation and deep visibility into receivables, FinFloh ensures you always know where your money is—and how to get it faster.

Whether you’re using accounts receivable financing or optimizing collections, FinFloh helps you maximize efficiency and reduce delays.

Talk to our experts or book a demo to see how you can unlock cash flow faster with smarter receivables management.