Credit scoring evaluates risk.

Credit decisions act on it.

While scoring measures probability, decisioning determines:

- Credit limits

- Payment terms

- Contract terms

- Pricing terms

- Approvals and holds

AI in credit decisions transforms these decisions from manual approvals into intelligent, policy-driven actions embedded directly into CRM workflows.

Table of Contents

What Is AI in Credit Decisioning?

AI in credit decisioning uses predictive risk models, workflow automation, and real-time data to recommend or execute credit actions automatically.

Instead of waiting for manual approvals, AI supports or automates decisions such as:

- Approving new customers

- Adjusting credit limits

- Customizing payment, pricing, or contract terms

- Triggering holds or structured onboarding paths

This ensures consistency, agility, and governance across your credit function.

Challenges in Traditional Credit Decision Processes

Many organizations still depend on:

- Manual spreadsheet-driven approvals

- Email-based review chains

- Static annual credit policies

- Siloed credit and sales processes

These limitations lead to:

- Slow customer onboarding

- Inconsistent credit offers

- Delayed revenue realization

- Higher exposure risk

AI resolves these by embedding intelligence into every credit decision.

How AI Improves Credit Decisions

Dynamic Credit Limit Management

AI continuously evaluates:

- Real-time payment behavior

- Outstanding exposure

- Risk score shifts

- Order growth trends

- Industry and macro signals

This enables credit limits to evolve with actual customer risk.

Contract Term Recommendations

Instead of generic contract terms, AI can analyze:

- Customer risk profile

- Historical payment behavior

- Order patterns

- Market risk signals

…and recommend contract terms such as:

- Minimum order sizes

- Escalation clauses

- Credit buffers

- Prepayment requirements

This aligns contract structure with real risk — minimizing exposure.

Pricing Term Recommendations

AI can also recommend pricing adjustments based on risk signals and buyer behavior, including:

- Early payment discounts

- Risk-adjusted pricing tiers

- Revenue-linked contracts

- Incentives for on-time payment

These dynamic pricing terms help sales teams strike deals quicker without sacrificing financial discipline.

Policy-Driven Automation

AI integrates with rule engines to enforce:

- Risk thresholds

- Exposure caps

- Approval hierarchies

- Escalation logic

Low-risk decisions can be auto-approved, and high-risk cases route for expert review.

Early Warning Triggers

When risk signals change — such as deteriorating payment trends — AI can:

- Recommend credit limit reductions

- Suggest revised payment terms

- Flag accounts for review

- Automatically update contract or pricing guidance

Measurable Business Outcomes

Organizations that apply AI in credit decisions benefit from:

- Faster sales onboarding

- Lower bad debt

- Higher revenue capture

- Consistent credit risk governance

- Better compliance and audit trails

Credit decisions become both faster and more disciplined.

Why AI in Credit Decisions Matters Today

In an environment of economic uncertainty and fast-moving markets:

- Exposure can change quickly

- Manual reviews don’t scale

- CRM and sales productivity suffer

AI ensures decisions align with risk appetite and business goals in real time.

How FinFloh Implements AI in Credit Decisions

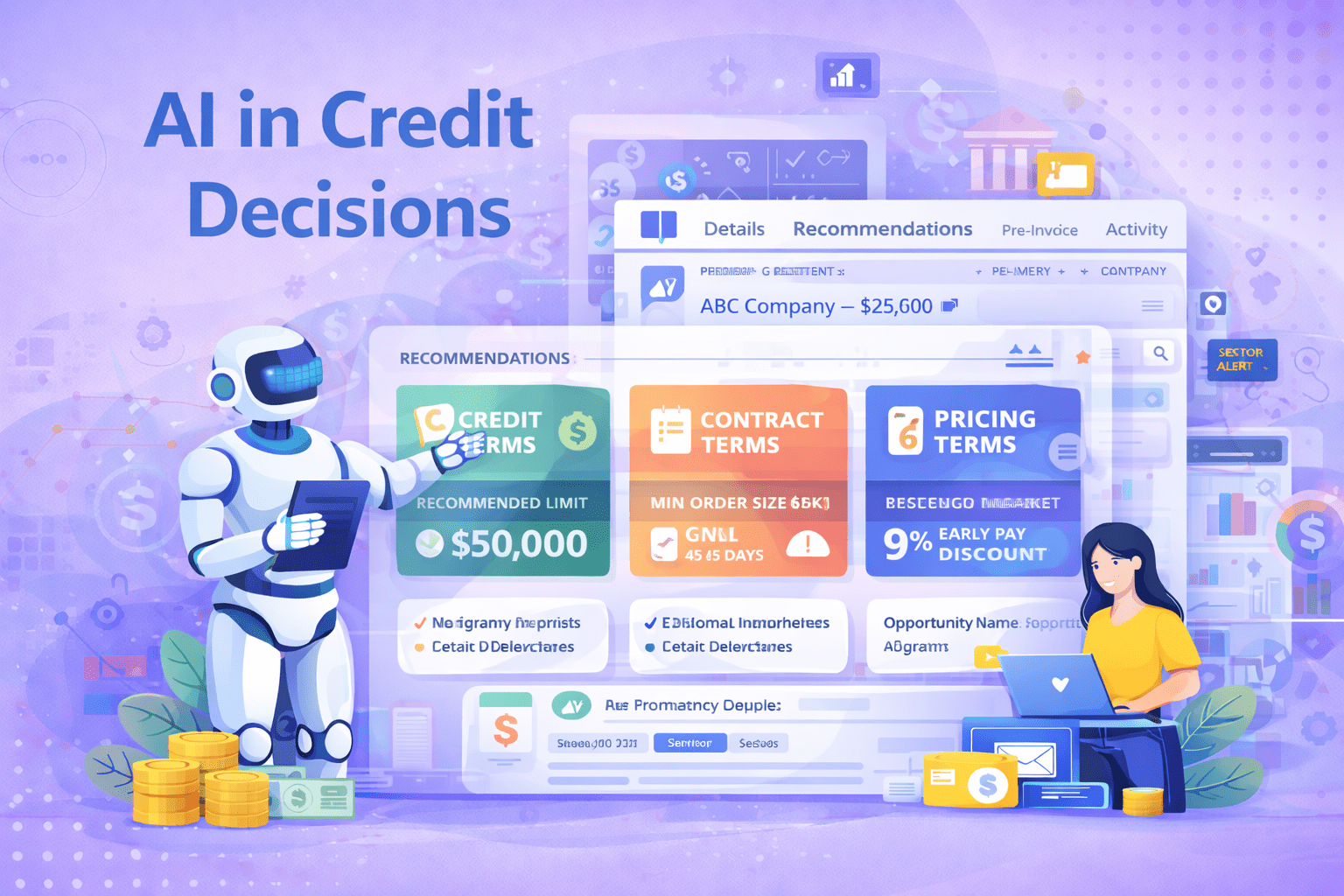

FinFloh’s AI-powered credit decisioning engine is embedded directly in CRM environments like Salesforce, enabling real-time credit, contract, and pricing recommendations exactly where deals are managed.

Real-Time, CRM-Embedded Decisioning

FinFloh analyzes buyer behavior, payment history, credit scores, and live risk signals to generate credit, contract, and pricing term recommendations at the opportunity stage — before a deal closes. This removes latency from traditional finance review cycles.

This means:

- Sales receive recommended credit limits

- Suggested payment terms (e.g., Net 30, early pay discount windows)

- Contract term guidelines

- Pricing term adjustments tied to risk and revenue objectives

All without switching applications.

Integrated Market Intelligence

FinFloh enriches decisioning with external signals such as:

- Industry risk trends

- Order volatility

- Macroeconomic indicators

This ensures that credit decisions reflect both customer data and market context — a major advantage in volatile markets.

Automated Onboarding & Rapid Approvals

By connecting to CRM workflows, FinFloh can:

- Accelerate onboarding of new accounts

- Auto-recommend credit and contract packages

- Trigger alerts for finance review

- Reduce reliance on manual spreadsheets and email approvals

This leads to faster sales cycles and lower friction between credit and sales.

To implement FinFloh’s AI Engine for Credit Decisions, you can check out FinFloh Credit Decisions product page. You can also Book a Demo to see how the product works or you can Book a Free Trial for a first-hand experience of the product.

Conclusion

AI in credit decisions is more than just automation.

It is about aligning risk, contract, pricing, and revenue objectives in real time.

Powered by Machine Learning, CRM integration, and market intelligence, AI ensures the right customers receive the right terms — accelerating growth without compromising financial stability.