For most businesses, accounts receivable represents one of the largest sources of expected cash inflow. Yet many finance teams only recognize cash flow problems after payments are already delayed, disputes have escalated, or liquidity pressure begins affecting operations.

The reality is that receivables often show warning signs long before serious cash flow issues emerge.

Customer payment behavior, collections patterns, disputes, and invoice activity can reveal early indicators of financial stress and collection risk. Organizations that identify these signals early can improve forecasting accuracy, reduce bad debt exposure, and protect working capital more effectively.

Modern finance teams are increasingly shifting from reactive collections management to proactive receivables risk monitoring.

Table of Contents

Why Receivables Are a Leading Indicator of Cash Flow Risk

Cash flow problems rarely appear suddenly.

In many cases, warning signs emerge gradually through:

- Slower payments

- Increased disputes

- Broken payment commitments

- Changing customer behavior

- Rising overdue balances

Receivables data provides one of the earliest operational views into potential liquidity disruptions.

This is why CFOs, treasury leaders, and AR teams are paying closer attention to receivables intelligence.

Common Early Warning Signals in Receivables

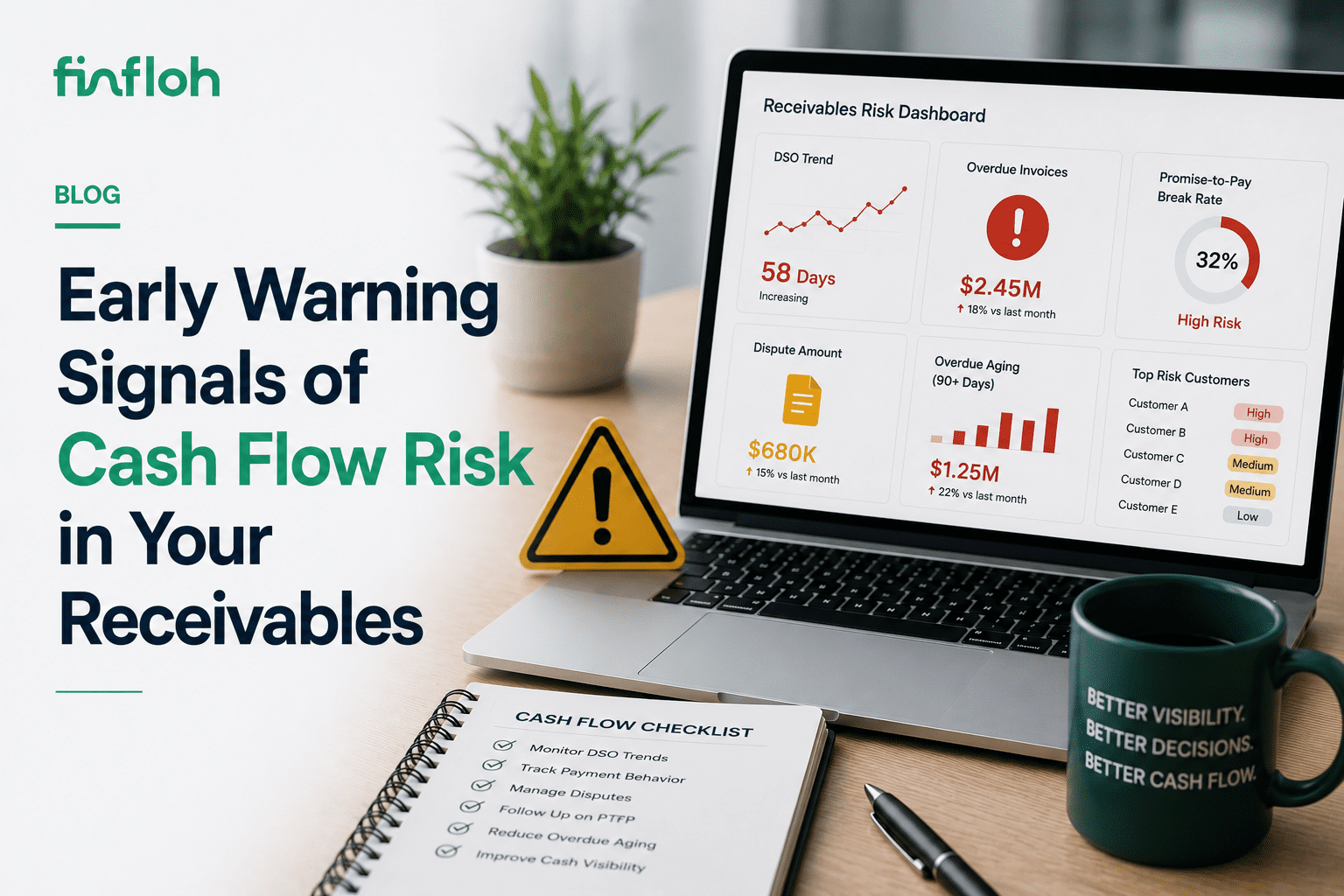

1. Increasing Days Sales Outstanding (DSO)

A rising DSO trend is one of the clearest indicators of weakening collection performance.

If customers are taking longer to pay:

- Cash conversion slows

- Working capital pressure increases

- Liquidity forecasting becomes less reliable

Even small increases in DSO can significantly impact available cash across large invoice volumes.

2. Customers Consistently Paying Beyond Terms

Some customers gradually extend payment cycles over time.

For example:

- Net 30 customers begin paying in 45 days

- Net 45 customers shift toward 60+ days

These behavioral shifts may indicate:

- Internal approval bottlenecks

- Customer cash flow pressure

- Deteriorating financial health

3. Rising Promise-to-Pay Break Rates

Promise-to-pay (PTP) commitments provide direct insight into customer payment intent.

When customers repeatedly miss committed payment dates, it may signal:

- Financial stress

- Operational instability

- Prioritization of other creditors

Broken PTP patterns are often early indicators of collection risk.

4. Increasing Invoice Disputes and Deductions

A sudden increase in:

- Invoice disputes

- Pricing disagreements

- Short payments

- Deduction claims

can delay collections and reduce forecast reliability.

Disputes may also reflect:

- Customer cash preservation tactics

- Internal operational breakdowns

- Relationship deterioration

5. Growing Overdue Aging Buckets

An increase in invoices moving into:

- 60+ days overdue

- 90+ days overdue

- 120+ days overdue

indicates rising collection risk and worsening liquidity exposure.

The longer invoices remain unpaid, the lower the probability of timely recovery.

6. Increased Partial Payments

Customers making partial payments instead of settling invoices fully may be attempting to manage limited cash availability.

Partial remittances often create:

- Reconciliation complexity

- Collection delays

- Forecast uncertainty

7. Slower Response to Collections Communication

When customers become:

- Less responsive to emails

- Difficult to contact

- Delayed in acknowledging invoices

- Unclear about payment timelines

this may indicate operational or financial stress.

8. Sudden Changes in Payment Patterns

Unexpected shifts in payment behavior can be strong early warning signals.

Examples include:

- Previously reliable customers delaying payments

- Customers requesting revised payment terms

- Increased payment rescheduling requests

Behavioral changes often matter more than static credit ratings.

9. Customer Concentration Risk

If a large portion of receivables depends on a few customers, any payment disruption can significantly impact liquidity.

Concentration risk becomes especially dangerous when:

- Large customers delay payments

- Key accounts experience financial stress

- Industry-specific slowdowns occur

10. High Volumes of Unapplied Cash

Unapplied or unmatched payments reduce visibility into actual receivables status.

This creates:

- Forecast inaccuracies

- Reporting confusion

- Delayed collections follow-ups

High unapplied cash volumes often indicate operational inefficiencies that affect liquidity visibility.

Why Traditional Receivables Monitoring Falls Short

Many organizations still rely on:

- Monthly AR aging reports

- Static dashboards

- Manual spreadsheets

- Historical payment averages

These approaches are reactive rather than predictive.

Modern cash flow management requires continuous monitoring of operational payment signals.

Why CFOs and Treasury Teams Are Paying Attention

Receivables are no longer viewed only as a collections function.

Today’s CFOs recognize that receivables behavior directly impacts:

- Liquidity planning

- Cash flow forecasting

- Working capital optimization

- Borrowing needs

- Financial risk exposure

This is driving closer integration between AR, treasury, and credit management teams.

The Role of AI in Detecting Receivables Risk

AI is helping finance teams identify cash flow risks earlier and more accurately.

Behavioral Pattern Analysis

AI models analyze:

- Payment timing trends

- Customer behavior changes

- PTP adherence

- Collection interactions

- Dispute frequency

to detect emerging risks.

Predictive Risk Scoring

Dynamic risk models continuously adjust customer risk profiles using live operational data.

Forecasting Optimization

AI improves forecasting by incorporating:

- Real-time collections activity

- Customer communication signals

- Payment behavior patterns

Early Warning Alerts

Systems automatically flag customers likely to:

- Delay payments

- Miss commitments

- Escalate disputes

- Increase overdue balances

Why Early Detection Matters

Identifying cash flow risk early allows finance teams to:

- Prioritize collections efforts

- Adjust liquidity plans

- Reassess customer exposure

- Reduce bad debt risk

- Improve working capital control

The earlier risks are detected, the more options organizations have to respond proactively.

How FinFloh Helps Detect Receivables Risk Early

FinFloh helps finance teams improve receivables visibility through intelligent AR workflows and predictive insights.

Real-Time Receivables Monitoring

Track:

- Aging trends

- Collection performance

- Customer payment behavior

- Overdue exposure

through centralized dashboards.

Promise-to-Pay Visibility

Monitor customer payment commitments and identify delayed or broken promises early.

Integrated Dispute Tracking

Gain visibility into dispute-related collection risks and aging impact.

Predictive Collections Insights

AI-driven insights help identify emerging payment risks and forecasting disruptions.

Unified Invoice-to-Cash Visibility

FinFloh connects invoicing, collections, disputes, and payment tracking into one receivables intelligence environment.

To understand how to monitor and optimize the receivables risk, you can check out FinFloh Credit Hub product and FinFloh Collections product page. You can also Book a Demo to see how it works.

Best Practices for Monitoring Receivables Risk

Track Behavioral Changes

Monitor shifts in payment behavior—not just overdue balances.

Monitor PTP Reliability

Measure how consistently customers honor payment commitments.

Review Aging Trends Continuously

Identify customers with worsening overdue patterns early.

Integrate Treasury and AR Visibility

Ensure treasury teams have access to operational receivables insights.

Use Predictive Analytics

Move beyond static reporting toward dynamic risk monitoring.

The Future of Receivables Risk Management

Finance organizations are increasingly moving toward predictive receivables intelligence.

Instead of reacting to missed payments after they occur, businesses are using:

- AI-driven forecasting

- Real-time payment monitoring

- Dynamic customer risk scoring

- Operational payment signals

to anticipate liquidity disruptions earlier.

Receivables are becoming a strategic source of treasury and working capital intelligence.

Conclusion

Cash flow risk often begins inside receivables long before it appears in financial statements or treasury reports.

Delayed payments, broken commitments, disputes, and changing customer behavior all provide early warning signals that finance teams can use proactively.

Organizations that monitor receivables intelligence continuously will improve:

- Forecast accuracy

- Liquidity visibility

- Collections effectiveness

- Working capital control

- Financial resilience

In modern finance operations, receivables are no longer just operational data—they are one of the earliest indicators of future cash flow risk.