Credit scoring has traditionally relied on static financial statements, bureau reports, and manual judgment.

But in today’s volatile environment, internal data alone is not enough.

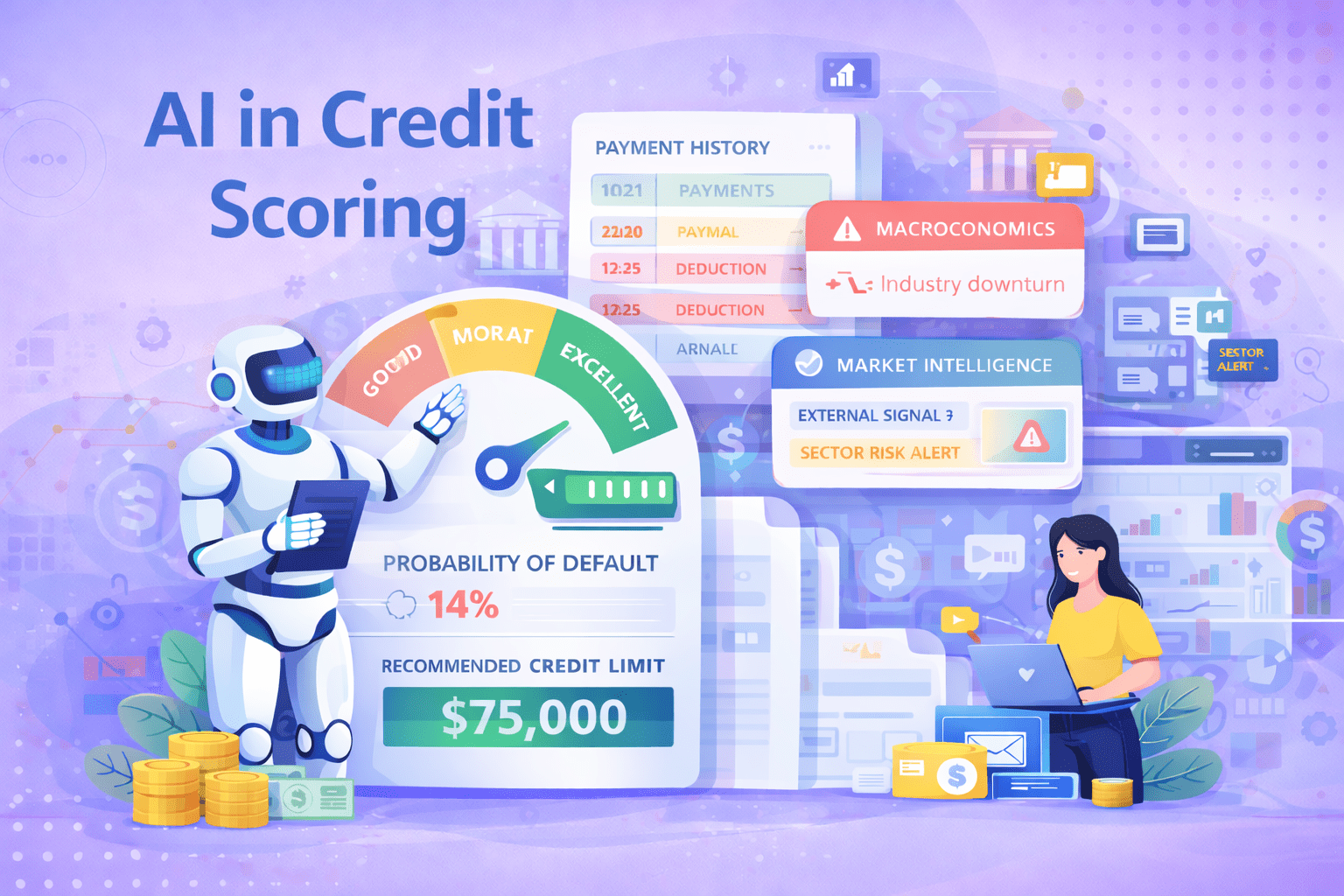

AI in credit scoring — powered by Machine Learning (ML) and enriched with Market Intelligence — enables finance teams to move from backward-looking evaluation to real-time, predictive risk management.

Table of Contents

What Is AI in Credit Scoring?

AI in credit scoring uses Machine Learning (ML) algorithms, behavioral analytics, and both internal and external data signals to assess the probability that a customer will:

- Pay on time

- Delay payments

- Default

- Increase dispute or deduction behavior

Unlike traditional models that rely on fixed formulas, ML models continuously learn from payment behavior, transaction history, and external risk signals.

The result is more accurate, adaptive, and forward-looking credit scores.

Why Traditional Credit Scoring Falls Short

Traditional credit scoring typically depends on:

- Historical financial statements

- Bureau scores

- Trade references

- Manual underwriting

These approaches are:

- Updated infrequently

- Limited to backward-looking data

- Slow to reflect market shifts

- Dependent on subjective review

By the time traditional scores indicate deterioration, exposure may already be high.

The Role of Market Intelligence in Credit Scoring

Market Intelligence refers to external signals that reflect broader economic, industry, and customer-level risk trends.

These may include:

- Industry slowdown indicators

- Sector-specific stress signals

- Public financial disclosures

- Payment trend benchmarks

- Macroeconomic indicators

- Regional risk patterns

Why Market Intelligence Is Critical

Internal payment behavior shows how a customer has performed.

Market intelligence shows what may happen next.

For example:

- A customer paying on time today may operate in an industry experiencing rapid decline.

- A sector-wide liquidity crunch may increase systemic risk.

- Rising interest rates may affect leveraged businesses disproportionately.

Without market intelligence, credit scoring becomes incomplete.

With it, scoring becomes contextual and predictive.

How Machine Learning (ML) Enhances Credit Scoring

Real-Time Multi-Source Data Integration

ML models integrate:

- Internal payment history

- Invoice aging trends

- Deduction frequency

- Order volatility

- Industry risk indicators

- Macroeconomic signals

Scores dynamically update as both internal and external conditions change.

Behavioral Pattern Recognition

Machine Learning detects subtle risk signals such as:

- Gradual increase in payment delays

- Rising dispute frequency

- Partial payment behavior

- Reduced order volume

These signals often indicate financial stress before formal defaults occur.

Predictive Probability Modeling

Instead of assigning a static rating, ML calculates:

- Probability of late payment

- Probability of default

- Risk-adjusted exposure

- Expected loss projections

This enables more precise and proactive credit governance.

Continuous Learning and Adaptation

As new payments, disputes, and market signals emerge, ML models update automatically.

Credit scoring becomes a living, continuously improving system.

Business Impact of ML and Market Intelligence in Credit Scoring

Organizations leveraging both internal ML models and external market intelligence typically achieve:

- Lower bad debt

- Reduced unexpected defaults

- Faster onboarding approvals

- Improved risk-adjusted credit limits

- Better working capital protection

Risk becomes measurable in real time and contextualized within broader market conditions.

Why This Matters More Today

Global economic volatility, industry disruptions, and rising capital costs increase uncertainty.

Finance leaders need:

- Early warning systems

- Real-time exposure visibility

- Industry-level risk context

- Predictive insights, not just historical analysis

Combining ML with market intelligence delivers that visibility.

How FinFloh Implements ML and Market Intelligence in Credit Scoring

FinFloh embeds Machine Learning and market intelligence directly into its credit-to-cash intelligence backbone.

Dynamic ML-Based Risk Scoring

FinFloh analyzes:

- Customer payment history

- Aging patterns

- Deduction behavior

- Order volatility

- Industry risk trends

Risk scores update dynamically as conditions evolve.

Market-Aware Risk Contextualization

FinFloh enriches internal scoring with:

- Industry-level intelligence

- Sector performance signals

- Broader market risk indicators

This ensures credit decisions reflect not just customer behavior — but market conditions.

Early Warning Risk Alerts

When ML detects deteriorating patterns or sector stress, FinFloh triggers:

- Risk alerts

- Credit review workflows

- Exposure recalibration recommendations

Risk mitigation becomes proactive rather than reactive.

Unified Credit Visibility

Because FinFloh connects credit scoring with collections and cash application:

- Exposure reflects real-time posting

- Aging is accurate

- Credit limits align with current risk

Finance teams operate with a single intelligence layer across the entire credit-to-cash cycle.

The Outcome with FinFloh

With ML-powered, market-aware credit scoring, organizations can:

- Extend credit confidently

- Reduce exposure surprises

- Optimize credit limits dynamically

- Improve working capital stability

- Balance growth with risk discipline

To implement FinFloh’s AI Engine for Credit Scoring, you can check out FinFloh Credit Scoring product page. You can also Book a Demo to see how the product works or you can Book a Free Trial for a first-hand experience of the product.

Conclusion

AI in credit scoring is no longer just about internal payment history.

The combination of Machine Learning and Market Intelligence transforms scoring from static evaluation into dynamic risk intelligence.

The companies that adopt this approach will not only reduce bad debt — they will make smarter, faster credit decisions in an unpredictable world.